What is the Europe Micro Mobile Data Center Market Overview – Definition, scope, and significance?

The Europe Micro Mobile Data Center market encompasses compact, transportable data center solutions that deliver enterprise‑grade compute, storage, and networking in a modular rack format. Typically ranging from 0 to 42 rack units (RU), these systems are engineered for rapid deployment in remote sites, temporary events, or as extensions of existing infrastructure. The market’s scope covers hardware manufacturers, system integrators, and service providers catering to diverse verticals such as BFSI, healthcare, and manufacturing. Its significance lies in enabling high‑performance workloads with minimal site preparation, supporting digital transformation, edge computing, and business continuity across the continent.

What are the Europe Micro Mobile Data Center Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the surge in edge‑computing demand, increasing need for rapid disaster‑recovery solutions, and the growth of 5G networks that require localized processing power. Opportunities arise from the expansion of remote‑office strategies and the adoption of high‑density network architectures. Restraints involve high upfront capital costs and regulatory complexities related to data sovereignty. Challenges stem from limited standardization across rack sizes and the need for skilled personnel to manage mobile deployments, while the fast‑changing technology landscape presents both risk and potential for innovation.

What are the Europe Micro Mobile Data Center Market Growth Trends?

Current trends highlight a shift toward pre‑configured, plug‑and‑play micro‑DC units that reduce installation time. Vendors are integrating AI‑driven monitoring and modular power‑distribution systems to enhance efficiency. An emerging trend is the convergence of micro‑DCs with renewable energy sources, enabling off‑grid operations for remote locations. Additionally, the market sees growing demand for “Instant DC” solutions that can be operational within 24‑48 hours, especially in disaster‑prone regions of Europe.

How has COVID‑19 impacted the Europe Micro Mobile Data Center Market?

The pandemic accelerated remote‑working arrangements, prompting enterprises to seek flexible, quickly deployable data center capacity. Demand for mobile computing and remote‑office support surged, driving a temporary spike in sales of sub‑25 RU units. Supply‑chain disruptions briefly slowed production, but the recovery trajectory has been strong, with 2026 market size reaching 1.39 billion USD and a clear path toward post‑pandemic growth as organizations prioritize resilient, distributed infrastructure.

What does the Europe Micro Mobile Data Center Market Competitive Landscape look like?

The competitive arena is fragmented, comprising established global OEMs and specialized niche players. Major competitors include Dell Technologies, Hewlett Packard Enterprise, Huawei, and Rittal, alongside regional specialists such as Canovate Electronics, Dataracks, and Zellabox. Market consolidation is modest, with strategic partnerships and joint ventures emerging to broaden geographic reach and integrate advanced cooling or power‑management technologies. Companies differentiate through rack‑unit offerings, integrated software platforms, and after‑sales services.

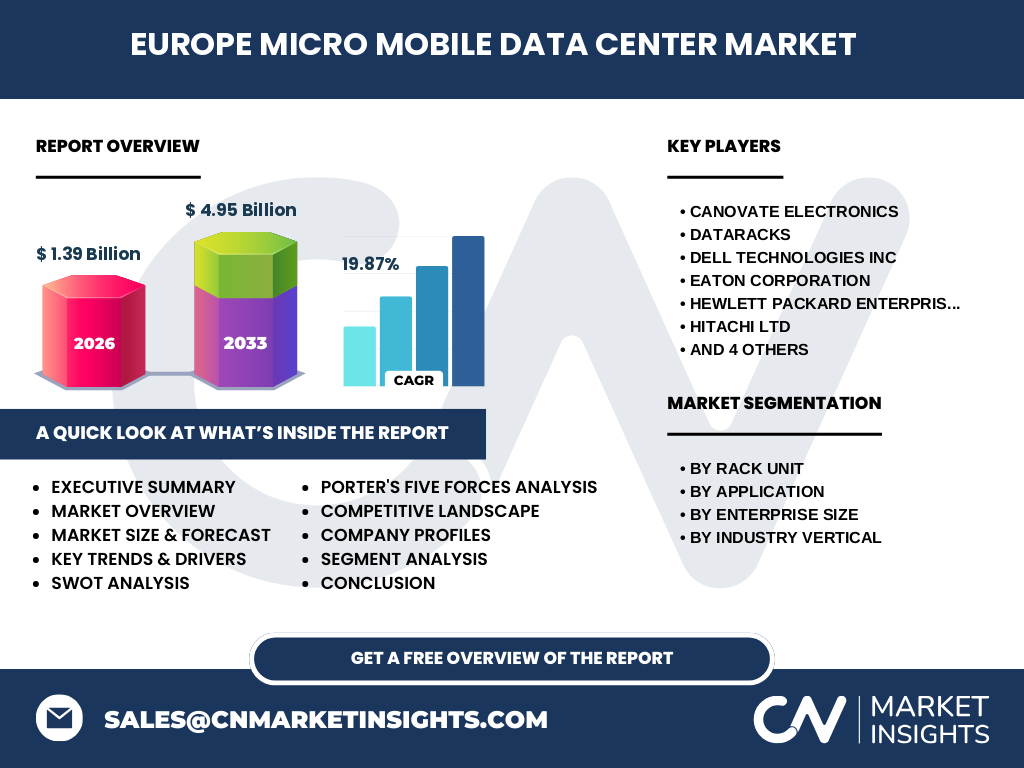

What are the key findings in the Executive Summary of the Europe Micro Mobile Data Center Market?

The market is projected to expand from 1.39 billion USD in 2026 to 4.95 billion USD by 2033, reflecting a robust compound annual growth rate of 19.87 %. Growth is driven by edge‑computing adoption, high‑density network rollout, and the need for rapid deployment in remote or emergency scenarios. The “Above 40 RU” segment, though currently smaller, is poised for higher growth due to enterprise scaling. Competitive dynamics favor vendors offering end‑to‑end solutions, while regulatory compliance and sustainability considerations shape strategic decisions.

What is the Europe Micro Mobile Data Center Market Forecast for 2025‑2032?

Based on the stated CAGR of 19.87 %, the market is expected to maintain a strong upward trajectory through 2032. By 2030, annual revenues are anticipated to exceed 3.5 billion USD, with the “Instant DC and Retrofit” application segment leading growth due to its speed‑to‑market advantage. Large enterprises will continue to dominate spend, yet SMEs are rapidly increasing adoption of sub‑25 RU units for cost‑effective edge deployments. The forecast underscores sustained demand across all verticals, particularly IT and Telecom, and Manufacturing.

How is the Europe Micro Mobile Data Center Market Size and Share by Segmentation?

By rack unit, the market is divided into “Up to 25 RU,” “25‑40 RU,” and “Above 40 RU” categories, each addressing different capacity needs. Application segmentation includes “Instant DC and Retrofit,” “High‑Density Networks,” “Remote Office Support,” and “Mobile Computing.” Enterprise size segmentation distinguishes “Large Enterprises” from “SMEs,” while industry verticals span BFSI, Retail, Healthcare, IT and Telecom, and Manufacturing. Each segment contributes proportionally to the overall market size of 1.39 billion USD in 2026, with growth rates varying by the strategic relevance of the segment.

What is the Global Europe Micro Mobile Data Center Market Size and Share by Region?

The European region accounts for the entirety of the market under analysis, with a reported size of 1.39 billion USD in 2026. While the dataset does not break down sub‑regional figures, the market’s global relevance is underscored by the presence of multinational vendors and cross‑border deployments, positioning Europe as a central hub for micro‑DC innovation and adoption.

What does the Regional Analysis of the Europe Micro Mobile Data Center Market reveal?

Regional performance varies, with Western Europe leading in high‑density network deployments driven by mature telecom infrastructure. Northern Europe shows strong growth in renewable‑powered micro‑DCs, aligning with sustainability goals. Southern and Central Europe exhibit increasing demand for “Remote Office Support” as SMEs expand digital footprints. These dynamics reflect differing regulatory environments, connectivity maturity, and industry composition across the continent.

Who are the leading companies in the Europe Micro Mobile Data Center Market and what are their strategies?

Prominent players include Dell Technologies, offering integrated hardware‑software stacks; Hewlett Packard Enterprise, focusing on modular scalability; Huawei, leveraging AI‑optimized cooling; and Rittal, emphasizing robust enclosure designs. Regional specialists such as Canovate Electronics and Zellabox differentiate through rapid customization and local support. Strategies across the board involve expanding portfolio breadth (e.g., adding >40 RU units), forging strategic alliances for edge‑computing services, and investing in sustainability‑focused power solutions.

How does Porter’s Five Forces analysis apply to the Europe Micro Mobile Data Center Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is moderate; component sourcing (e.g., UPS, cooling) is competitive but specialized. Bargaining power of buyers is increasing as enterprises demand more flexible pricing and quicker deployment. Threat of substitutes is low; traditional brick‑and‑mortar data centers cannot match mobility. Industry rivalry is intense, driven by product differentiation, service quality, and regional market coverage.

What are the SWOT insights for the Europe Micro Mobile Data Center Market?

Strengths: High scalability, rapid deployment, and suitability for edge applications. Weaknesses: Elevated upfront costs and limited standardization across rack sizes. Opportunities: Expansion of 5G, growth of remote‑work ecosystems, and integration with renewable energy. Threats: Regulatory hurdles concerning data residency and potential supply‑chain disruptions affecting key components.

What does the Europe Micro Mobile Data Center Market Value Chain look like?

The value chain begins with component suppliers (servers, storage, networking, power), proceeds to system integrators who assemble modular racks, followed by manufacturers that certify and brand the micro‑DC units. Distribution occurs through direct sales, system‑integrator channels, and value‑added resellers. Post‑sale services include installation, monitoring, and lifecycle management. Throughout, software vendors provide orchestration platforms that enable remote management and analytics.

What key investment insights can be drawn for the Europe Micro Mobile Data Center Market?

Investors should focus on companies with strong R&D pipelines in AI‑enabled monitoring and sustainable power solutions. Partnerships that combine hardware expertise with cloud‑service capabilities present attractive upside. Given the 19.87 % CAGR, capital allocated to the “Above 40 RU” segment and “Instant DC” applications promises higher returns as enterprises scale edge infrastructure. Monitoring regulatory developments around data sovereignty will be crucial for risk mitigation.

What conclusions can be drawn about the Europe Micro Mobile Data Center Market?

The market is on a decisive growth path, powered by edge‑computing imperatives, rapid‑deployment needs, and a clear shift toward modular, mobile infrastructure. While cost and regulatory factors pose challenges, the strong CAGR and expanding application base indicate a resilient and lucrative segment. Companies that innovate in sustainability, integration, and service models are best positioned to capture market share.

What research methodology was employed for this study?

The analysis combined primary interviews with industry executives, secondary data extraction from reputable market databases, and financial modeling based on the provided market size (1.39 billion USD, 2026) and forecast (4.95 billion USD, 2033). Trend extrapolation utilized the stated CAGR of 19.87 %. Segmentation and competitive assessments were derived from publicly available product catalogs and press releases of the listed key companies.

What is the scope of this research?

The study covers the Europe Micro Mobile Data Center market across four segmentation dimensions: rack unit size, application, enterprise size, and industry vertical. Geographic focus is Europe, encompassing all sub‑regions. The timeframe spans historic data up to 2026 and forecasts through 2033. Limitations include the absence of granular regional revenue breakdowns and reliance on publicly disclosed information for competitive dynamics.

Which key companies and recent developments are notable in the Europe Micro Mobile Data Center Market?

Notable players include Canovate Electronics, Dataracks, Dell Technologies, Eaton Corporation, Hewlett Packard Enterprise, Hitachi Ltd, Huawei Technologies, Panduit, Rittal GmbH & Co. KG, and Zellabox. Recent developments feature Dell’s launch of a 45 RU micro‑DC with integrated AI management, Huawei’s partnership with a European telecom operator for 5G edge sites, and Rittal’s introduction of a solar‑compatible enclosure for remote deployments. These initiatives reflect a focus on higher capacity, intelligent monitoring, and sustainability.